# Payment Service Providers (PSPs)

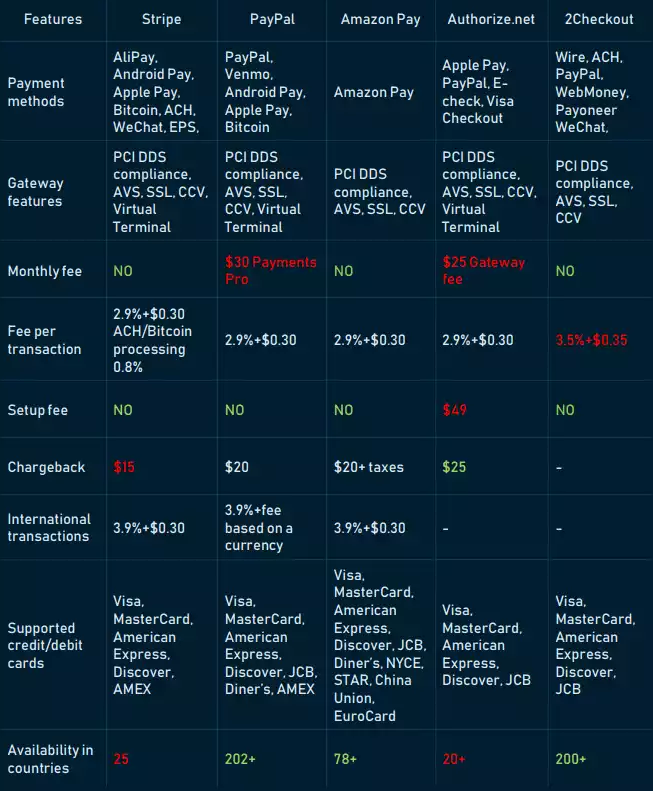

# Popular PSPs

# Types

# 1. Traditional Banks

- Role: Many banks offer payment processing services to their merchant customers, either directly or through partnerships with third-party PSPs.

- Advantages: Established trust, comprehensive financial services.

- Disadvantages: Potentially higher fees, slower onboarding process.

# 2. Independent PSPs

- Role: Standalone companies specializing in payment processing services.

- Advantages: Flexibility, advanced features, competitive pricing.

- Disadvantages: Might lack the comprehensive financial services of banks.

# 3. Payment Gateways

- Role: Focus solely on providing payment gateway services, enabling merchants to securely accept online payments.

- Advantages: Easy integration, wide range of payment options.

- Disadvantages: Limited to payment processing, additional services might be required.

# 4. Aggregators

- Role: Combine multiple payment methods and present them as a single solution to merchants.

- Advantages: Simplified integration, access to various payment options.

- Disadvantages: Potentially higher fees, less control over payment processing.

# 5. Merchant Acquirers

- Role: Handle the authorization and settlement of credit and debit card transactions.

- Advantages: Direct access to card networks, potential for lower fees.

- Disadvantages: Complex setup, higher operational costs.

# Additional Types**:

- Mobile Payment Processors: Specialize in processing payments made through mobile devices.

- E-wallet Providers: Offer digital wallet services for storing and transferring funds.

# Payment Processor vs. Payment Gateway

While both are essential components of electronic transactions, payment processors and payment gateways serve distinct roles.

# Payment Gateway

- The interface: A payment gateway is the online equivalent of a physical point-of-sale terminal.

- Collects information: It securely collects customer payment information (card number, expiration date, CVV).

- Transmits data: Encrypts and sends this information to the payment processor.

- Provides feedback: Communicates the transaction's approval or decline back to the merchant.

# Payment Processor

- The backend: Handles the complex process of routing and processing the transaction.

- Verifies information: Checks the validity of the payment information.

- Authorizes transaction: Communicates with the customer's bank to authorize the purchase.

- Transfers funds: Facilitates the transfer of funds from the customer's bank to the merchant's account.

- Fraud prevention: Implements security measures to protect against fraudulent transactions.

# Summarization

- Payment gateway: The customer-facing part of the transaction.

- Payment processor: The behind-the-scenes engine that makes it happen.

← Paypal notes Network →